Tom Price failed to repeal ObamaCare

He may rely heavily on Senator Rand Paul's plan. Posted on 2/12/2017 and updated on September 29, 2017.

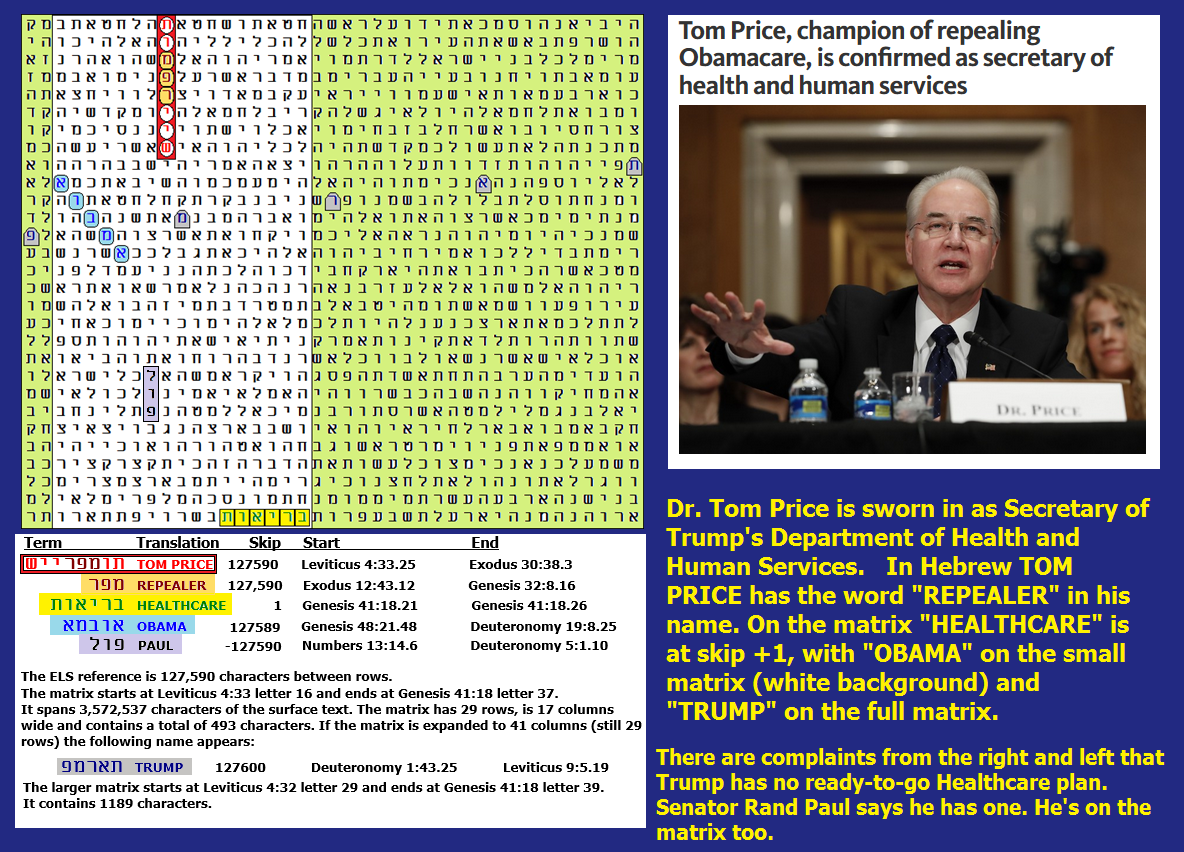

On February 12, 2017 I wrote that "TOM PRICE is the axis term on this matrix. Dr. Tom Price, as our new Secretary of Health and Human Services will not only repeal ObamaCare, but in Hebrew three sequential letters in his name – mem peh resh – actually mean REPEALER. On this matrix we find one of the three times in Torah that HEALTHCARE is at skip +1. There is an ELS of OBAMA at one skip less than TOM PRICE. In the presidential primaries one of the men that Trump humiliated was Senator Rand Paul. After President Trump took office it soon appeared that the Trump Administration had no ready-to-go replacement for ObamaCare, but Senator Paul does claim to have one. It remains to be seen if Paul's plan is adopted, but PAUL is at the same absolute skip as TOM PRICE and REPEALER. All this is seen in a 493-letter matrix. When the matrix is expanded to 1,189 letters there is an ELS of TRUMP."

Oops, TOM PRICE may have had REPEALER in his name, but what got repealed was him as Secretary of Health and Human Services. Neither Price nor Paul succeeded in repealing and replacing OnamaCare. Prices resigned for abusing use of Government aircraft.

What does Senator Paul's Healthcare plan look like? There is a look at it in the Daily Caller. The report is as follows:

Sen. Rand Paul Introduces Obamacare Replacement plan

By Juliegrace Brufke

2:39 PM 01/25/2017

GOP Kentucky Sen. Rand Paul introduced his Obamacare replacement plan Tuesday, calling on Republican lawmakers to “repeal and replace” the legislation simultaneously.

Under the proposal, individual and employer mandates would be eliminated while popular provisions from the Affordable Care Act — including allowing dependents to stay on their parents’ health care plans until the age of 26 and requiring insurers to cover preexisting conditions — would remain intact.

Those with preexisting conditions would be given a two-year open enrollment period to get covered, and those who don’t purchase coverage during that window could then purchase coverage through a group market.

The plan includes a provision aimed at evening the playing field for those who don’t receive their coverage through their employer by providing a tax credit up to $5,000 for contributions made to their health savings accounts.

If enacted, Paul’s proposal would establish Independent Health Pools (IHPs), allowing individuals to pool together to purchase insurance plans. The Public Health Service Act (PHSA) would also be amended to allow individuals to pool together to obtain health benefits coverage through IHPs.

The plan would also allow individuals to purchase care across state lines, which is intended to increase competition and drive down costs.

Paul has been vocal about his call to repeal and replace quickly, a sentiment shared by President Donald Trump and House Speaker Paul Ryan.

“Getting government out of the American people’s way and putting them back in charge of their own health care decisions will deliver a strong, efficient system that doesn’t force them to empty out their pockets to cover their medical bills,” Paul said in a statement. “There is no excuse for waiting to craft an alternative until after we repeal Obamacare, and the Obamacare Replacement Act charts a new path forward that will insure the most people possible at the lowest price.”

STATISTICAL SIGNIFICANCE OF THE MATRIX. As per my standard protocol, no statistical significance is assigned to the axis term, here a transliteration of TOM PRICE at its 17th lowest skip in wrapped Torah. Before considering the ELS rank, odds against finding HEALTHCARE at SKIP +1 were about 206 to 1 on the 493-letter segment of the matrix with the white background, but the odds drop to about 85.9 on the full 1,189 letter full matrix. Due to similar drops in values with other a priori terms when moving from the small matrix to the full matrix, and due to the fact that one of two 5-letter spellings of Trump had a 16.75% chance to be found on a 1,189-letter matrix, the expansion to the full matrix is not justified. To show TRUMP the overall statistical value drops from one chance in 820 to one chance in 237. This turned out to be the only really significant a priori term. Again, he was involved in it, but failed to repeal it. What follows is what I originally wrote on this topic.

So the focus must be on the small matrix. On it I found that the odds against having in the 493 letters was about 7.16 to 1, HOWEVER, this allows no extra value for the fact that the real area was not 493-letters for the match of TOM PRICE with REPEALER. The real area was just 8 letters because, for whatever reason, TOM PRICE spelled tav vav mem peh resh yud yud sin includes the 3 letter term sought for REPEALER: mem peh resh. My method of odds evaluation does not award extra value for location unless the axis term and a priori terms are at pre-specified angles as is the case with ELS maps that point to where I believe the Ark of the Covenant is found in the northern Sinai desert of Egypt. There is an ELS of OBAMA at skip 125,589, one skip less than TOM PRICE at skip 127, 590. Although the term stands out because each letter of Obama touches another, the term is diagonal rather than vertical or horizontal, and is thus not counted as a special case skip (skip +/- 1 or the absolute skip of the axis term). Odds in favor of finding one of two spellings accepted for Obama were high - about 48%, and thus the term is not overly significant although it only takes 12 letters to show TOM PRICE, REPEALER and OBAMA. As for having PAUL at a special case skip, the odds against this find were a bit under 5 to 1. Overall, after factoring in ELS rank 17 of the axis term, the odds against the smaller matrix were about 820. It will be interesting to return to this matrix once a replacement for Obamacare is passed and to compare what the new law looks like with respect to what Rand Paul espouses. However, we already know that Trump, like Paul, favors allowing dependents to stay on their parents’ health care plans until the age of 26 and requiring insurers to cover preexisting conditions as well as allowing individuals to purchase care across state lines.